Securing funding for a small business can feel like navigating a labyrinth. Traditional loans often come with stringent requirements and lengthy approval processes‚ leaving many entrepreneurs searching for viable alternatives. The good news is that innovative financing options are constantly emerging‚ offering flexible and accessible pathways to fuel growth. This article explores four alternative ways to fund your small business that can help you overcome financial hurdles and achieve your entrepreneurial dreams. These strategies move beyond the conventional‚ providing opportunities for businesses of all sizes to thrive and prosper by carefully considering alternative ways to fund your small business.

1. Bootstrapping: The Power of Self-Reliance

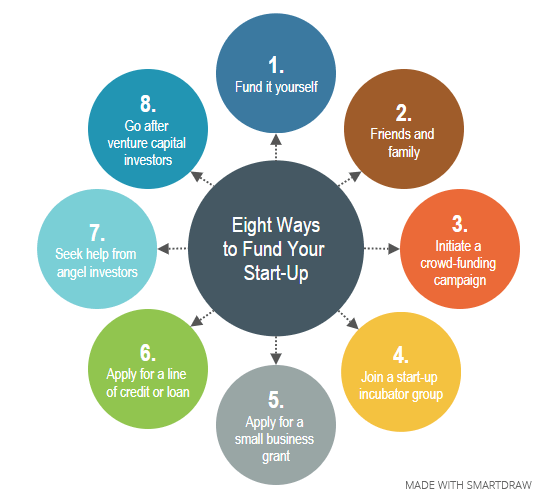

Bootstrapping‚ or self-funding‚ is the most common method for startups. It involves using your own savings‚ personal loans‚ and revenue generated from the business itself to finance operations. While it requires a strong commitment and a frugal mindset‚ bootstrapping allows you to retain full ownership and control of your company.

Advantages of Bootstrapping:

- Complete control over your business decisions.

- No debt or equity dilution.

- Forces you to be resourceful and efficient;

- Demonstrates commitment to potential investors.

Disadvantages of Bootstrapping:

- Limited access to capital‚ slowing growth.

- High personal risk.

- Can be stressful and demanding.

- May miss out on opportunities due to lack of funds.

2. Crowdfunding: Harnessing the Power of the Crowd

Crowdfunding platforms like Kickstarter and Indiegogo allow you to raise capital from a large number of individuals in exchange for rewards‚ equity‚ or simply donations. This approach is particularly effective for businesses with compelling stories‚ innovative products‚ or a strong community following.

Types of Crowdfunding:

- Reward-based: Backers receive a product‚ service‚ or experience in return for their contribution.

- Equity-based: Investors receive equity in the company in exchange for their investment.

- Debt-based: Borrowers receive a loan from backers‚ which is repaid with interest.

- Donation-based: Backers contribute without expecting anything in return.

3. Invoice Factoring: Unlocking Cash Flow from Outstanding Invoices

Invoice factoring‚ also known as accounts receivable financing‚ involves selling your outstanding invoices to a factoring company at a discount. The factoring company provides you with immediate cash‚ and then collects payment from your customers. This can be a valuable solution for businesses with long payment cycles.

How Invoice Factoring Works:

- You sell your invoices to a factoring company.

- The factoring company pays you a percentage of the invoice value (typically 70-90%).

- The factoring company collects payment from your customers.

- Once the customer pays‚ the factoring company pays you the remaining balance‚ minus their fees.

4. Microloans: Small Loans‚ Big Impact

Microloans are small loans‚ typically ranging from $500 to $50‚000‚ offered by non-profit organizations and community development financial institutions (CDFIs). These loans are often easier to qualify for than traditional bank loans and can be used for a variety of purposes‚ such as working capital‚ equipment purchases‚ or inventory.

Benefits of Microloans:

- Lower barriers to entry than traditional loans.

- Often come with mentorship and support services.

- Can help build credit history.

- Support local communities.

FAQ: Funding Your Small Business

Q: What is the best alternative funding option for my business?

A: The best option depends on your specific needs‚ industry‚ and financial situation. Consider your risk tolerance‚ cash flow requirements‚ and long-term goals.

Q: How do I choose a crowdfunding platform?

A: Research different platforms and compare their fees‚ features‚ and target audience. Choose a platform that aligns with your project and business goals.

Q: What are the risks of invoice factoring?

A: The risks include high fees‚ potential damage to customer relationships‚ and the loss of control over your accounts receivable.

Q: Where can I find microloan providers?

A: Search online for CDFIs and non-profit organizations in your area that offer microloans.

Securing funding for a small business can feel like navigating a labyrinth. Traditional loans often come with stringent requirements and lengthy approval processes‚ leaving many entrepreneurs searching for viable alternatives. The good news is that innovative financing options are constantly emerging‚ offering flexible and accessible pathways to fuel growth. This article explores four alternative ways to fund your small business that can help you overcome financial hurdles and achieve your entrepreneurial dreams. These strategies move beyond the conventional‚ providing opportunities for businesses of all sizes to thrive and prosper by carefully considering alternative ways to fund your small business.

Bootstrapping‚ or self-funding‚ is the most common method for startups. It involves using your own savings‚ personal loans‚ and revenue generated from the business itself to finance operations. While it requires a strong commitment and a frugal mindset‚ bootstrapping allows you to retain full ownership and control of your company.

- Complete control over your business decisions.

- No debt or equity dilution.

- Forces you to be resourceful and efficient.

- Demonstrates commitment to potential investors.

- Limited access to capital‚ slowing growth.

- High personal risk.

- Can be stressful and demanding.

- May miss out on opportunities due to lack of funds.

Crowdfunding platforms like Kickstarter and Indiegogo allow you to raise capital from a large number of individuals in exchange for rewards‚ equity‚ or simply donations. This approach is particularly effective for businesses with compelling stories‚ innovative products‚ or a strong community following.

- Reward-based: Backers receive a product‚ service‚ or experience in return for their contribution.

- Equity-based: Investors receive equity in the company in exchange for their investment.

- Debt-based: Borrowers receive a loan from backers‚ which is repaid with interest.

- Donation-based: Backers contribute without expecting anything in return.

Invoice factoring‚ also known as accounts receivable financing‚ involves selling your outstanding invoices to a factoring company at a discount. The factoring company provides you with immediate cash‚ and then collects payment from your customers. This can be a valuable solution for businesses with long payment cycles.

- You sell your invoices to a factoring company.

- The factoring company pays you a percentage of the invoice value (typically 70-90%).

- The factoring company collects payment from your customers.

- Once the customer pays‚ the factoring company pays you the remaining balance‚ minus their fees.

Microloans are small loans‚ typically ranging from $500 to $50‚000‚ offered by non-profit organizations and community development financial institutions (CDFIs). These loans are often easier to qualify for than traditional bank loans and can be used for a variety of purposes‚ such as working capital‚ equipment purchases‚ or inventory.

- Lower barriers to entry than traditional loans.

- Often come with mentorship and support services.

- Can help build credit history.

- Support local communities.

A: The best option depends on your specific needs‚ industry‚ and financial situation. Consider your risk tolerance‚ cash flow requirements‚ and long-term goals.

A: Research different platforms and compare their fees‚ features‚ and target audience. Choose a platform that aligns with your project and business goals.

A: The risks include high fees‚ potential damage to customer relationships‚ and the loss of control over your accounts receivable.

A: Search online for CDFIs and non-profit organizations in your area that offer microloans.

Beyond the Basics: Advanced Considerations for Alternative Funding

While the aforementioned methods represent frequently employed alternatives to traditional lending‚ a more nuanced understanding of the funding landscape necessitates consideration of additional strategies and key factors influencing their suitability. These advanced considerations can prove instrumental in optimizing capital acquisition and fostering long-term financial stability.

Strategic Partnerships and Joint Ventures

Establishing strategic partnerships or engaging in joint ventures with complementary businesses can provide access to both capital and valuable resources. This collaborative approach allows for the sharing of costs‚ expertise‚ and market access‚ effectively mitigating financial risk and accelerating growth trajectories. Due diligence is paramount; thoroughly vet potential partners and ensure alignment in strategic objectives and operational practices. The legal framework governing such partnerships should be meticulously drafted to protect the interests of all parties involved.

Government Grants and Subsidies

Numerous government agencies offer grants and subsidies specifically designed to support small business development. These programs often target specific industries or demographics‚ providing non-dilutive funding that does not require repayment. The application process can be competitive and time-consuming‚ demanding meticulous documentation and a compelling articulation of the business’s social and economic impact. Resources such as Grants.gov and the Small Business Administration (SBA) website provide comprehensive listings of available programs.

Venture Capital and Angel Investors: A High-Growth Trajectory

For businesses exhibiting significant growth potential‚ seeking investment from venture capitalists or angel investors can provide substantial capital infusions. However‚ this path involves relinquishing a portion of equity and ceding some degree of control over business decisions. Thoroughly research potential investors‚ focusing on their track record‚ industry expertise‚ and investment philosophy. A well-crafted business plan‚ financial projections‚ and a compelling pitch deck are essential for attracting investor interest. Legal counsel is crucial throughout the negotiation process to ensure fair terms and protect the company’s long-term interests.

Factoring vs. Asset-Based Lending: A Comparative Analysis

| Feature | Invoice Factoring | Asset-Based Lending |

|---|---|---|

| Collateral | Accounts Receivable (Invoices) | Inventory‚ Equipment‚ Real Estate |

| Focus | Short-term cash flow | Larger‚ longer-term financing needs |

| Creditworthiness | Primarily based on customer credit | Based on the borrower’s creditworthiness and asset value |

| Advance Rate | Typically 70-90% of invoice value | Varies depending on asset type and value |

| Cost | Factoring fee based on invoice volume and collection period | Interest rates and fees based on asset value and loan terms |

Understanding the nuances of each funding option is paramount. While invoice factoring offers immediate liquidity by leveraging accounts receivable‚ asset-based lending provides larger‚ longer-term financing secured by tangible assets. The choice between these methods depends on the specific financial needs and asset base of the business.

In the ever-evolving landscape of small business finance‚ adaptability and informed decision-making are paramount. By embracing a holistic approach that considers both conventional and unconventional funding sources‚ entrepreneurs can significantly enhance their prospects for success. It is imperative that business owners conduct thorough due diligence‚ seek expert financial advice‚ and carefully evaluate the terms and conditions associated with each funding option before committing to a particular course of action. This strategic approach to financing will empower businesses to navigate the complexities of the capital markets and achieve sustainable growth. The final thought is that‚ the successful application of these strategies depends on a comprehensive understanding of your company’s specific needs and long-term objectives; therefore‚ choosing the optimal path to securing alternative ways to fund your small business requires careful consideration.